In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

OPIS

Wafer prices continued to trend downward, marking the fourth consecutive week of declines and highlighting manufacturers’ increasing reliance on price concessions to stimulate sales and ease mounting inventory and cash flow pressures, according to market participants.

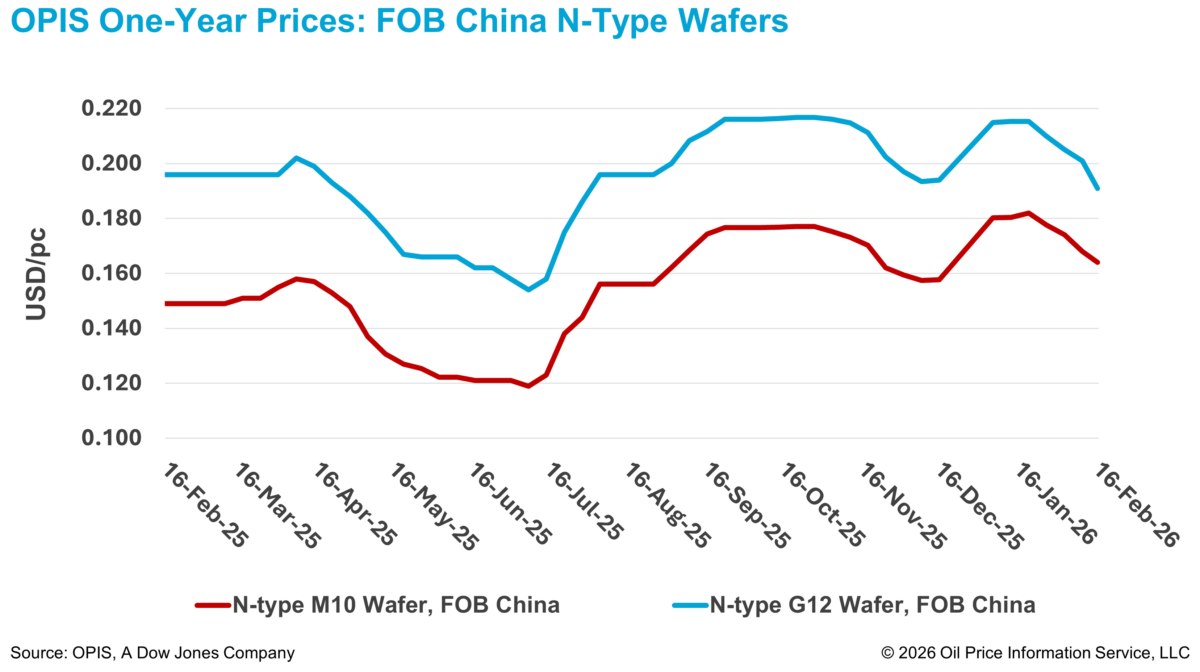

Free-On-Board (FOB) China prices for n-type M10 and n-type G12 wafers declined week on week by 2.38% and 4.98%, to $0.164/pc and $0.191/pc, respectively, according to the OPIS Global Solar Markets Report released on February 16.

The broader wafer market environment remains subdued and largely passive, characterized by weak trading activity and ongoing inventory accumulation, according to market sources. The photovoltaic installation market’s seasonal slowdown has directly weakened downstream demand for upstream production materials, while elevated manufacturing costs at the downstream level have further constrained buyers’ ability to absorb current wafer prices.

According to industry feedback last week, operating rates at major wafer producers have fallen below 50%. Even specialized wafer manufacturers, which traditionally maintained utilization rates of up to 80%, have seen operating rates decline to below 70%. A market observer noted that the broad-based reduction in operating rates suggests prices have fallen to levels that are no longer economically sustainable for manufacturers.

Nevertheless, some market participants indicated that downstream operating rates are likely to recover after the Lunar New Year, as certain cell and module producers still have outstanding orders to fulfill. This could lead to a modest rebound in post-holiday wafer procurement volumes. However, a trading source cautioned that the potential impact on prices may be limited, given that current wafer inventories are estimated at approximately 25 GW.

Financial pressure on wafer manufacturers remains significant. This is highlighted by the January 2026 edition of the mainstream photovoltaic product cost analysis recently released by the China Photovoltaic Industry Association. The assessment estimated the tax-inclusive full production cost of n-type G12R wafers at CNY 1.945 ($0.28)/pc in January 2026. In contrast, according to industry sources, the prevailing domestic transaction price for this wafer specification in China currently stands at approximately CNY 1.2–1.3/pc, indicating substantial margin compression.

A market participant noted that while the pricing reference of the China Photovoltaic Industry Association (CPIA) functions more as guidance than as a binding standard, it may nonetheless influence market sentiment. In particular, it could provide psychological price support, potentially helping to slow the pace of declines and contribute to short-term stabilization.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Popular content