By Michael Kern – Mar 09, 2026, 6:00 PM CDT

- The coordinated closure of the Strait of Hormuz and the Bab el-Mandeb Strait has triggered a dual-chokepoint crisis, crippling global shipping and resulting in massive, immediate cost increases for oil, LNG, and maritime insurance.

- Beyond the immediate energy shock, the crisis is causing a critical fertilizer shortage due to a halt in Gulf production and shipping, which is predicted to result in a severe decline in crop yields and higher grocery bills months later.

- This war-driven shock, layered on top of existing political and tariff uncertainty, is projected to accelerate global inflation and threatens to tip major world economies into stagflation due to the simultaneous disruption of multiple transmission channels like energy, shipping, and air cargo.

I want to talk about the thing nobody in Washington seems willing to say out loud, which is that the cost of this war is going to show up at your kitchen table before it shows up in any congressional budget hearing.

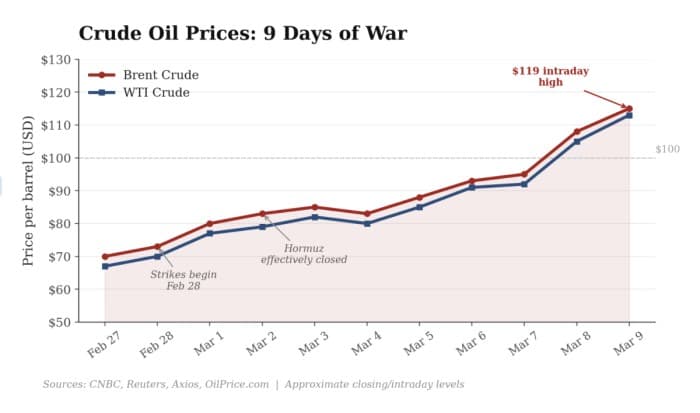

This morning oil prices blew past $115 a barrel. Brent crude touched $119 overnight before pulling back. WTI posted its biggest weekly gain in the entire history of futures trading, dating back to 1983.

The S&P futures are down.

The Nikkei dropped 5% at open.

South Korea’s KOSPI cratered 6%.

The VIX is at levels we haven’t seen since Trump’s “Liberation Day” tariff tantrum last April.

And the President of the United States went on Truth Social last night to call surging oil prices “a very small price to pay.”

He is, at this point, the only person in the world who thinks that.

So here’s where we are…

On February 28, the United States and Israel launched coordinated airstrikes on Iran…Operation Epic Fury, if you want the Pentagon branding…targeting military facilities, nuclear sites, and leadership.

The strikes killed Supreme Leader Ali Khamenei. Iran retaliated. Missiles hit U.S. bases in Qatar, the UAE, Bahrain. Drones struck a desalination plant in Bahrain, energy facilities in Saudi Arabia and Kuwait, and a fuel storage depot in Dubai’s Jebel Ali port. A dockworker was killed. Seven American service members have died.

As of this morning, Iran’s Assembly of Experts has named Mojtaba Khamenei, the dead Supreme Leader’s son, as his successor, which is the geopolitical equivalent of changing the nameplate on the door.

We are nine days into this war, and nobody’s stopping.

But I’m not writing about the war. Not really. I’m writing about what the war is doing to the invisible infrastructure of the global economy, the shipping lanes and insurance markets, fertilizer contracts, and airfreight corridors that nobody thinks about until they break.

Because they’re breaking right now, in ways that will take months to repair, and the people who will pay for it aren’t the ones making the decisions.

The Chokepoint

The Strait of Hormuz is 21 miles wide at its narrowest point. Through that gap moves roughly 20 percent of the world’s oil, about 20.9 million barrels per day. It also carries a significant share of global liquefied natural gas, a third of the world’s seaborne fertilizer exports, and a meaningful slice of container traffic linking Asia, Europe, and the Middle East.

It is, as of right now, essentially closed.

Not formally. Nobody has dropped a chain across it. But Iran’s Revolutionary Guard declared the waterway shut to allied shipping.

Protection and indemnity insurers pulled coverage. War-risk premiums, which had already tripled in the days before the strikes, became irrelevant once insurers stopped offering any coverage at all.

And without insurance, no shipowner will send a vessel through. It’s not the missiles that closed the Strait. It’s the actuarial tables.

Tanker traffic through the Strait of Hormuz has dropped from an average of 138 vessels per day to roughly two.

One hundred and fifty tankers are sitting at anchor in open Gulf waters.

One hundred and forty-seven container ships are trapped inside the Persian Gulf, unable to exit.

Maersk, CMA CGM, Hapag-Lloyd, MSC, every major container line, has suspended operations. Maersk paused two key services linking the Middle East to Asia and Europe and halted all trans-Suez sailings through the Bab el-Mandeb Strait.

The Houthis, who had eased up on Red Sea attacks in recent months, announced they’re resuming. So now both chokepoints are closed, and the only way around is the Cape of Good Hope, which adds 10 to 14 days to every voyage.

This is what a dual chokepoint crisis looks like. It’s never happened before in modern container shipping.

Let me put this in dollars.

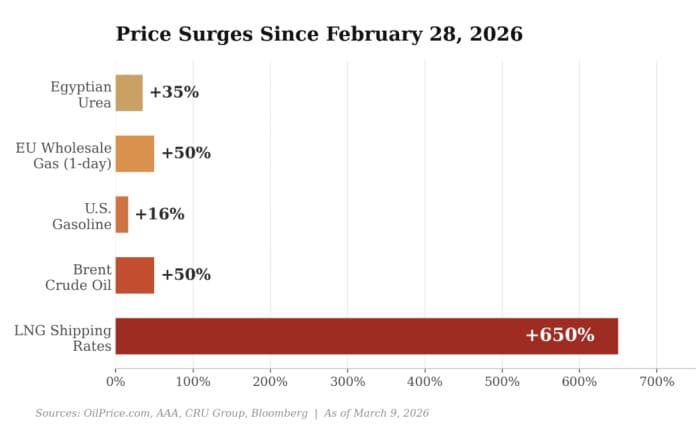

LNG shipping charter rates went from $40,000 a day to $300,000 a day in less than a week. That’s a 650 percent increase.

Asian spot LNG prices doubled.

Qatar halted all LNG production at its Ras Laffan hub, the largest LNG export complex on Earth, after Iranian drones hit facilities there, and declared force majeure on its contracts.

Qatar and the UAE together supply roughly 20 percent of the world’s LNG, and 85 percent of Qatar’s exports go to Asia.

China, India, Japan, South Korea, Taiwan, all scrambling for replacement cargoes from the United States, Australia, or West Africa, at multiples of the old price, on ships that now cost seven times more to charter.

European wholesale gas prices surged more than 50 percent in a single day, the biggest move since the Russia-Ukraine chaos of 2022.

The Asian LNG premium over European prices hit a multi-year high, indicating traders are routing every available molecule to Asia and squeezing Europe on the back end.

Energy Aspects director Amrita Sen put it plainly: “There’s no spare capacity in the LNG market.”

And this is just gas.

The Oil Shock You Were Promised You’d Never See Again

Crude oil has risen roughly 50 percent since February 28. That’s not a typo.

Brent was trading around $70 a barrel before the strikes. It touched $119 overnight.

WTI has moved from $67 to over $115.

Iraq, the second-largest OPEC producer, has seen output from its three main southern oilfields collapse by 70 percent, from 4.3 million barrels per day to 1.3 million, because there’s nowhere to put the oil.

Kuwait has cut production preemptively. The UAE is “carefully managing offshore production levels.”

Everyone in the Gulf is producing less because the tankers can’t get out.

Meanwhile, Israel struck a major fuel storage facility near Tehran over the weekend.

Saudi Arabia’s 550,000-barrel-per-day Ras Tanura refinery has been hit twice. Drones even targeted Saudi Aramco’s million-barrel-per-day Shaybah oil field.

We are watching the physical destruction of energy infrastructure in real time, which means this isn’t just a shipping problem. Even when the Strait reopens, some of this supply isn’t coming back quickly.

The average American gasoline price was around $3 a gallon before the strikes. As of Sunday, it’s $3.45, according to AAA—up 50 cents in a week.

Energy Secretary Chris Wright went on Fox News and said higher prices are “a small price to pay.”

The President echoed that.

Goldman Sachs published a worst-case scenario predicting $100 oil within five weeks. It happened in five days.

The Stuff Nobody’s Talking About

Here’s where it gets interesting, and by interesting I mean quietly devastating.

Fertilizer.

Modern agriculture runs on natural gas. Not metaphorically. Ammonia, the base ingredient in most nitrogen fertilizers, is synthesized from natural gas through the Haber-Bosch process.

A huge share of global ammonia and urea production is concentrated in the Gulf states, because that’s where the cheap gas is.

A third of the world’s seaborne urea exports move through the Strait of Hormuz. And the natural gas that powers fertilizer plants elsewhere—including in India, which depends heavily on Qatari LNG for its domestic urea production—also moves through the strait.

Egyptian urea prices have already shot up 35 percent this week. Sulphur prices are surging.

Nearly half of global sulphur trade originates in the Middle East. And this is hitting at the worst possible moment: spring planting season in the Northern Hemisphere, when farmers are making their purchasing decisions for the year.

Even modest reductions in nitrogen application produce disproportionately large declines in crop yield.

We’re not going to feel this at the grocery store next week. We’re going to feel it in September, when the harvests come in short.

Fertilizer shocks don’t register like oil shocks. Gas prices change overnight. Crop yields reveal themselves months later. But as The Conversation noted in an analysis this week, the latter may prove more destabilizing.

Air freight.

Airspace is closed or restricted across Iran, Iraq, Israel, Qatar, Kuwait, Bahrain, and parts of the UAE, Oman, and Saudi Arabia.

The European Aviation Safety Agency issued a bulletin advising operators not to fly over any of these countries at any altitude.

Over 20,000 flights have been grounded since February 28. More than a million people have been stranded. Global air cargo capacity has declined by 18 percent, and the Asia-Middle East-Europe corridor, which previously handled about half of all air freight from China to Europe, has seen capacity drop by 40 percent.

Middle Eastern carriers represent 13.6 percent of global air cargo capacity and most of their operations are offline.

This isn’t just about Amazon packages being late. Air cargo moves pharmaceuticals, electronics components, perishable goods, machine parts.

When a cargo consultant told The Register that “globally these represent a small portion of the market,” he was talking about tech products flowing through the UAE as a distribution hub. He was not talking about the kidney dialysis supplies that move on Emirates SkyCargo, or the semiconductor precursors that go through Doha.

The backlogs are building, warehouse capacity is straining, and every rerouted flight burns more fuel—fuel that now costs 30 percent more than it did two weeks ago.

Maritime insurance.

This is the hidden engine of the whole crisis. Before the strikes, war-risk insurance for a single transit of the Strait of Hormuz had already risen from 0.125 percent to 0.4 percent of a ship’s insured value. For a very large crude carrier, that’s an extra quarter of a million dollars per transit.

Then the insurers pulled coverage entirely. And without P&I coverage, ships cannot legally operate.

Inside North America’s First Fully Integrated Rare Earth Facility

It doesn’t matter if the U.S. Navy escorts you through, if you don’t have insurance, your cargo isn’t recognized at the destination port. The entire global shipping network runs on a layer of underwriting that most people never think about, and that layer just evaporated in the Gulf.

War risk surcharges of $1,500 to $3,500 per container have been imposed on everything touching the Middle East.

MSC declared “end of voyage” on stranded shipments, which shifts responsibility, and cost, to the cargo owner. VLSFO, the fuel most container ships burn, has climbed past $650 per metric ton. Marine gasoil broke $1,000 for the first time since late 2023.

Every one of these costs gets passed along.

The Tariff Problem on Top of the War Problem

And here’s the thing: this isn’t happening in a vacuum.

Two weeks before the bombs started falling, the Supreme Court handed down its ruling in Learning Resources v. Trump.

Six justices, including Chief Justice Roberts, held that the International Emergency Economic Powers Act does not authorize the President to impose tariffs.

Roberts wrote the opinion himself, 21 pages, delivered in 10 measured minutes from the bench, and it effectively struck down the entire architecture of Trump’s reciprocal tariff regime. The country-specific levies, the China duties, the fentanyl surcharges on Canada and Mexico—all of it, gone.

Trump’s response was immediate and predictable. He called the ruling “unfortunate” and “disappointing” at the State of the Union. Then he signed a proclamation invoking Section 122 of the Trade Act of 1974, a statute that had never been used before, to impose a new 10 percent global tariff, which he promptly announced he’d raise to 15 percent (the statutory maximum).

He directed his Trade Representative to launch “accelerated” investigations under Sections 232 and 301, covering everything from batteries to electrical grid equipment to plastics to pharmaceuticals.

Section 122 tariffs expire in 150 days unless Congress extends them.

That’s mid-July. Right around midterm season.

So now you’ve got a lame-duck tariff regime layered on top of the old Section 232 steel and aluminum duties, on top of the first-term Section 301 China tariffs that were never challenged, on top of pending new investigations, and all of it is feeding into a supply chain that’s simultaneously being rerouted around two closed maritime chokepoints and hit with war-risk surcharges.

FedEx has already filed suit to recover everything it paid under the illegal IEEPA tariffs.

Senate Democrats announced legislation demanding $175 billion in refunds to businesses.

China’s Ministry of Commerce called the ruling a vindication of its retaliatory strategy and maintained its restrictions on rare earth exports.

Mark Zandi at Moody’s Analytics summarized the situation with unusual bluntness: “The U.S. is pulling away from the world, and the rest of the world is now pulling away from the U.S.”

The Inflation Cascade

So let’s trace the logic. You have oil prices up 50 percent. LNG prices doubled. Shipping rates up 650 percent in the spot market. Container surcharges of thousands of dollars per box. Air cargo capacity down almost a fifth globally. Fertilizer prices surging at the start of planting season. And a tariff regime that, even in its diminished post-Supreme Court form, still adds 10 to 15 percent to the cost of most imports.

Before the war, U.S. core inflation was showing signs of easing.

The February CPI report, expected this Wednesday, is projected to show core inflation rising just 0.2 percent month-over-month. But that’s pre-war data.

It’s already stale.

Goldman Sachs estimated that if oil stays at current levels for several months, U.S. consumer price inflation could climb from 2.4 percent in January to 3 percent by year-end.

Capital Economics said most Asian economies would see inflation rise by half a percentage point.

The EU, already at 2 percent, could see a full percentage point added.

And those are the optimistic scenarios that assume the strait reopens relatively quickly.

The Federal Reserve is watching all of this. New York Fed president John Williams said the war would “obviously affect kind of a nearer-term inflation outlook.” Minneapolis Fed president Neel Kashkari, who had penciled in one rate cut this year, said the attacks made him less certain. Former Treasury Secretary Janet Yellen warned that tariffs alone could push inflation to 3 percent, and now you’re adding a war-driven energy shock on top of that.

Mortgage rates, which had been drifting lower, reversed course, back up to 6.13 percent on a 30-year fixed as of Thursday.

The logic is simple: higher expected inflation pushes up Treasury yields, which push up mortgage rates, which push out first-time homebuyers, which keeps the housing market locked.

Every $10 increase in oil prices adds roughly 25 cents to a gallon of gasoline.

Delta Air Lines said in its annual filing that a 1-cent increase in jet fuel per gallon costs the company $40 million a year.

A 10 percent increase? A billion dollars.

And then there’s China.

February CPI came in at 1.3 percent year-over-year, the highest in three years, blowing past the 0.8 percent consensus.

The Lunar New Year holiday helped, but gasoline prices rose 3.1 percent and gold jewelry surged 76.6 percent.

Factory-gate prices are still deflating, but at the slowest pace since mid-2024, partly because rising crude oil is putting a floor under industrial costs. Analysts warned that a prolonged conflict could tip the global economy into stagflation—that ugly combination where prices rise but growth doesn’t. China’s property slump, America’s tariff chaos, and a Middle Eastern war walk into a bar. Nobody’s laughing.

The Political Math

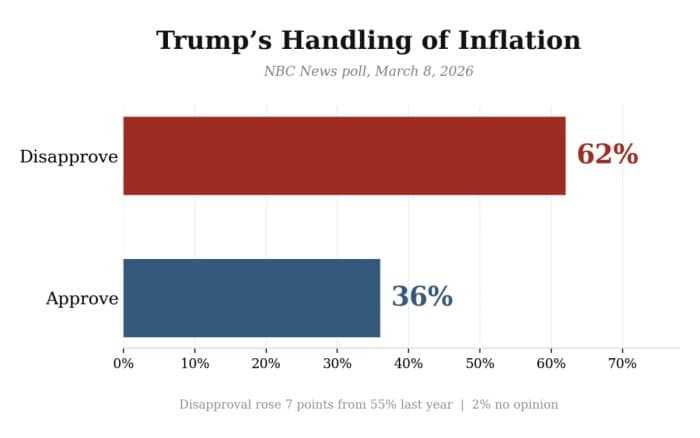

An NBC News poll released this weekend showed 62 percent of voters gave negative ratings to Trump’s handling of inflation—up 7 points from last year’s already-bad 55 percent. Nearly double the 36 percent who expressed support.

U.S. employers cut 92,000 jobs in February. The war is costing an estimated $1 billion a day, according to congressional sources.

Tim Pool—Tim Pool—a MAGA-aligned YouTuber, not exactly The Economist—said: “I oppose this war. The president will pay a political price.” He added that a significant number of people regret their vote, saying this feels like the Bush administration all over again.

A week ago, Trump stood before Congress and made the case that his economic agenda was working.

Gas prices down, stock market up, inflation slowing, mortgage rates dropping.

Four days later, he started bombing Iran and undid almost all of it.

His Energy Secretary went on television to say prices would come down in “weeks, certainly not months.”

The White House floated naval escorts for tankers. Treasury issued a 30-day sanctions waiver to let Indian refiners buy Russian oil as a stopgap. The administration offered political risk insurance to tankers, though the shipping industry appears unimpressed. None of this has worked. Oil kept climbing.

The G7 finance ministers held an emergency call this morning to discuss coordinated release of strategic petroleum reserves.

If that sounds familiar, it’s because it’s the same playbook from 2022, when Russia invaded Ukraine.

The difference is that in 2022, the Strait of Hormuz was open. The Red Sea was open. Container shipping was functioning. Air freight was flying. The global economy had shock absorbers. This time, we’re absorbing a shock that’s hitting every transmission channel simultaneously: energy, shipping, air cargo, insurance, fertilizer, financial markets, and trade policy. All at once.

I keep coming back to a phrase from a logistics consultant quoted in a trade publication last week: “One week of direct impact can easily translate into more than a month of structural disruption.”

That’s the part that gets lost in the daily oil price ticker.

Even if the Strait reopens tomorrow…which it won’t…you still have 147 container ships trapped in the Gulf that need to clear out.

You have port congestion cascading through every downstream hub.

You have carriers that declared force majeure and offloaded containers at random ports.

You have equipment stuck in the wrong hemisphere.

You have contracts voided and surcharges locked in and insurance premiums that won’t come down for months.

Qatar’s Energy Minister Saad al-Kaabi told the Financial Times that if the war continues, Gulf producers may be forced to halt exports entirely and that this “will bring down economies of the world.”

He is not being dramatic. He is describing what happens when a fifth of global energy supply is removed from a system that was already running without slack.

The LNG market had no spare capacity before the war. Container shipping was already stretched from two years of Red Sea diversions. Air cargo was operating with thin margins. Fertilizer prices were already elevated.

The global economy didn’t have a buffer, and now it’s absorbing the worst supply shock since the 1970s.

Chatham House noted that Qatar produces 40 percent of the world’s helium, used in semiconductor manufacturing. That’s another chokepoint nobody was tracking until the drones arrived.

The war will end at some point. Wars do. But the inflationary damage is already compounding in ways that the “short-term pain” framing cannot contain.

The farmer who can’t get urea in March doesn’t plant the same crop in April.

The airline that’s paying a billion extra in fuel costs doesn’t un-raise its fares in June.

The shipper who signed a war-risk surcharge doesn’t get a refund.

The mortgage buyer who got priced out at 6.13 percent doesn’t magically come back at 5.8. These costs embed. They compound. They become the new baseline.

And the man who ordered the strikes is on Truth Social, calling it a small price to pay.

Sixty-two percent of voters disagree.

By Michael Kern for Oilprice.com

More Top Reads From Oilprice.com

- Saudi Aramco Cuts Oil Output as Hormuz Crisis Chokes Exports

- Asia Outbids Other Regions for Fuel Cargoes as War Chokes Supply

- Why This War With Iran May Be Far Longer Than Markets Expect

Download The Free Oilprice App Today