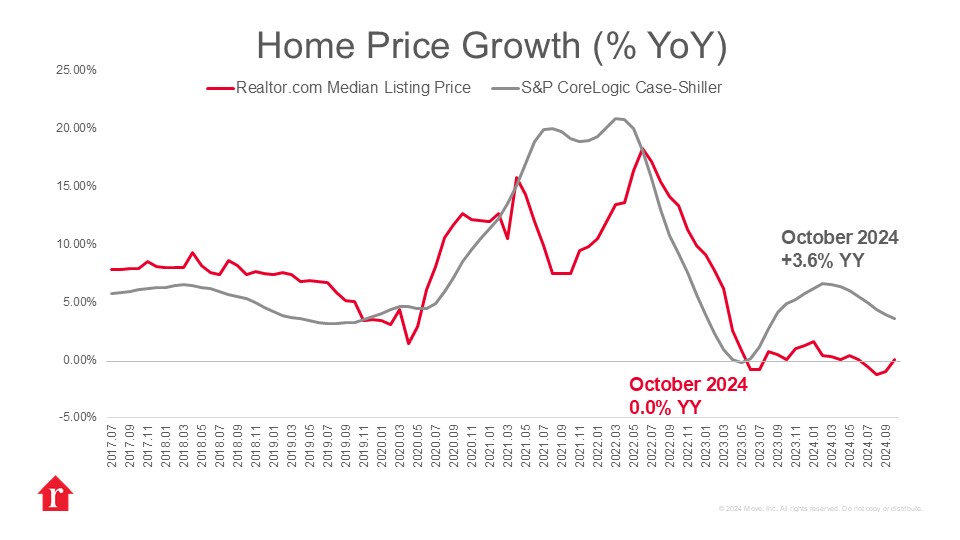

What does the data show?

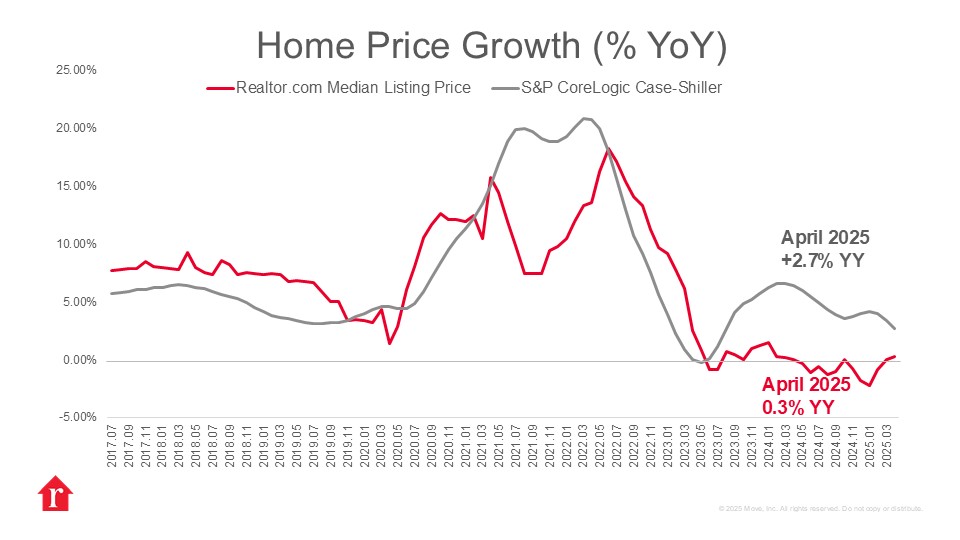

The S&P CoreLogic Case-Shiller Index increased 2.7% year over year in April. This is a slight decline from the March 2025 reading and the slowest annual gain since mid-2023. The 10-city index rose 4.1%, while the 20-city index had a 3.4% increase over the same period. This month’s release covers home sales in February, March, and April—a period where elevated mortgage rates and cautious consumer sentiment weighed on housing activity. Mortgage rates averaged above 6.8%, capping affordability just as the spring selling season began to ramp up.

How did trends vary by region?

As regional supply and demand dynamics continue to diverge, so do price trends. Price growth is expected to remain strongest in the Northeast and Midwest, where inventory is tightest and demand still exceeds supply. The Northeast and Midwest were led by New York, which saw a 7.9% increase, Chicago, with a 6% increase, and Detroit, with a 5.5% increase, on an annual basis. These areas are still experiencing demand that exceeds supply. By contrast, the Tampa and Dallas markets were the only two metros to post a year-over-year decline, reflecting a softening in formerly high-growth metros.

What is ahead for housing?

While more homes are coming to market compared with a year ago, high borrowing costs and affordability barriers are tempering buyer enthusiasm. Economic uncertainty and elevated rates are likely to keep housing activity slower than usual this spring.

Regional market strength will depend heavily on local inventory dynamics, which have been correlated with construction trends, and how mortgage rates evolve over the summer. Limited inventory continues to support prices, and future supply may be constrained. New construction activity fell to a five-year low in May. However, completions remained elevated, keeping near-term options available while hinting at longer-term shortages.

Stock: Reflection AI Signs $6.3 Billion Compute Deal")