REVEALED: How much YOU could lose if Reeves slashes tax relief on ISAs – pensioners MOST at risk

Rachel Reeves has set her eyes on tax free Isas in her latest bid to kickstart economic growth, reports have indicated.

The Chancellor has been exploring slashing tax relief on Isas, a popular saving tool that offers a low-risk investment and generates a return in interest which is tax free.

It’s all part of her efforts to spark growth in Britain which includes potentially unlocking billions stashed away in pensions.

By slashing tax relief on ISAs and therefore making them less attractive, people will be more inclined to spend the money or make riskier, but potentially more lucrative, investments.

Reeves met with City firms who claimed £300billion held in cash ISAs would yield better results if they were invested in riskier stocks and shares ISAs.

However, experts have warned much of that £300billion is held by pensioners who tend to opt for the low-risk Isa option.

Jordan Clark, a financial planner at Quilter said: “Older savers, in particular, tend to hold significant amounts in cash ISAs. The average Isa value at the end of 2021 to 2022 was around £9,477 for the 25 to 34 age group.”

“This is compared to around £63,365 in the 65 and over group. A Freedom of Information request from Lane Clark and Peacock also revealed that in 2019, 5.8 million over-65s held ISAs, with 3.4 million holding exclusively cash ISAs, totalling £87billion in these accounts.”

Any reform to these ISAs would disproportionately affect older folk, therefore.

How much could you lose if Reeves slashes the tax relief?

Currently, people can earn tax-free interest on up to £20,000 each year held in cash ISAs (this has been frozen until 2030).

How much you could lose if the tax relief was scrapped depends on what kind of ISA you have and the differing interest rates of each type.

The three main types are:

- Easy access: Meaning you can withdraw money at any time.

- Fixed rate: Meaning you lock your money away for a set period to earn a guaranteed interest rate.

- Cash lifetime Isa: Meaning you can save towards your first home or retirement.

Each will have a different interest rate set by the provider, usually a bank.

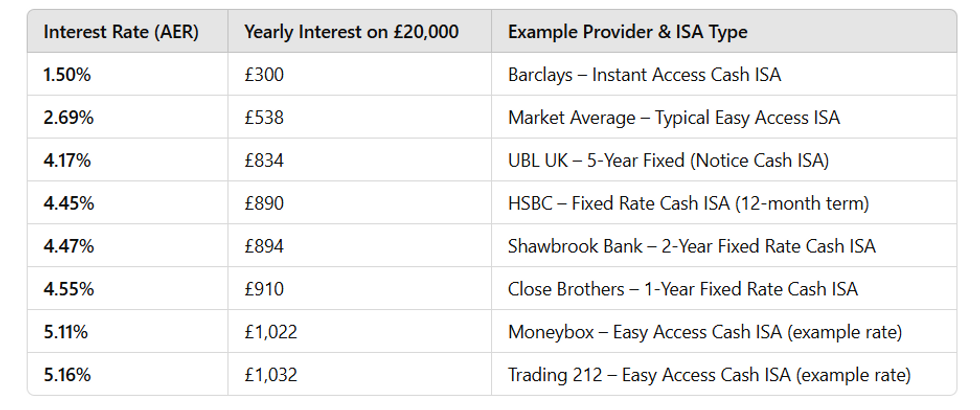

For example, if you had £20,000 in a more lucrative fixed rate ISA from HSBC who offer a 4.45 per cent interest rate, you would earn £890 per year, tax free.

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa

However, if Reeves scrapped the tax relief and imposed normal income tax on the interest earnings, these earnings would reduce significantly.

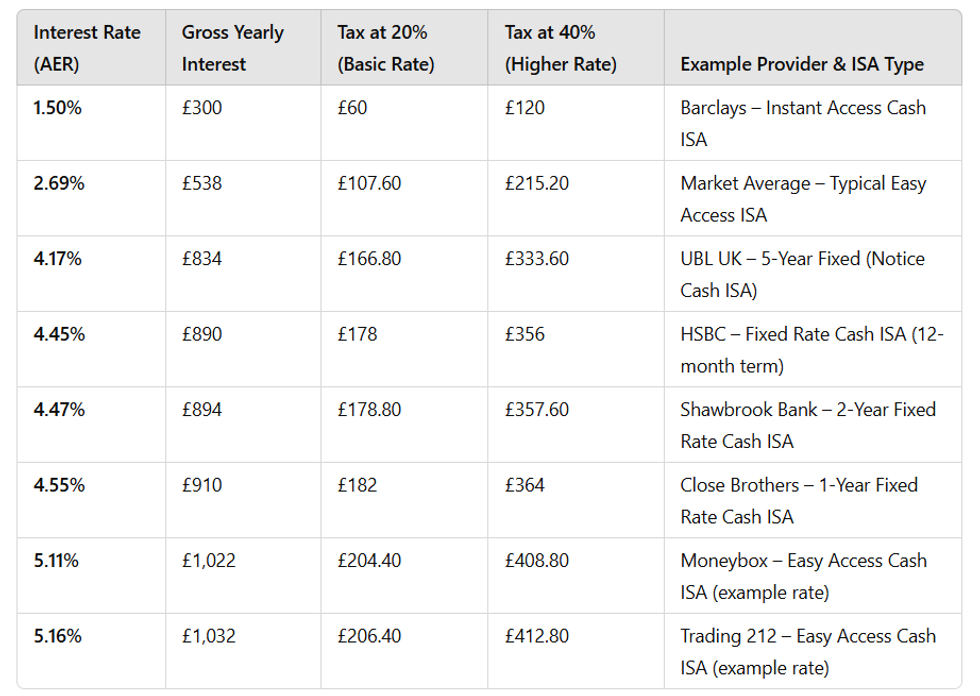

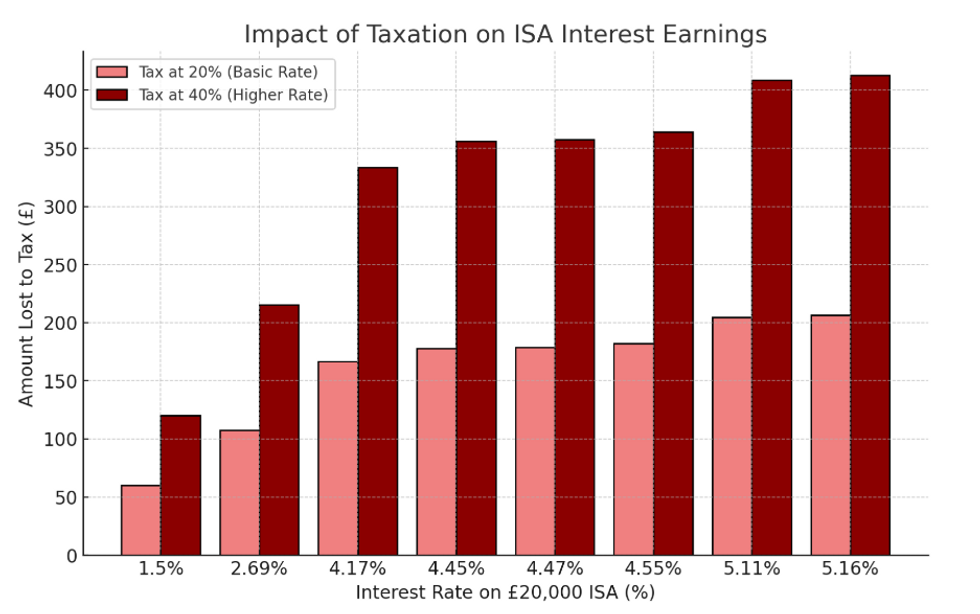

How much you would lose would depend on your income tax band. GB News has crunched the data and generated the following table showing how much your Isa would earn you and how much that earning would be reduced depending on your income tax band.

It reveals for people with £20,000 in a typical easy access Isa yielding 2.69 per cent in interest (market average), you would lose £107 a year if you were in the basic income tax band.

That rises to £215 a year lost to the Treasury if you are in the higher income tax band (40 per cent).

If you have a more lucrative Isa with a return of 4.45 per cent (as offered by HSBC), your earning of £890 a year from interest would be slashed by £178 if you are in the lower tax bracket and £356 if you are in the higher band.

LATEST FROM MEMBERSHIP:

- Trump’s tariffs tell us one crucial thing about his upcoming presidency – Roger Gewolb

- My dad was dragged from our pub by machete gang – there’s one way to solve knife crime – Adam Brooks

- HAVE YOUR SAY: Should Starmer be investigated for alleged Covid rule break? COMMENT NOW

How much you could lose if Isa earnings were subject to income tax, broken down via interest rate and tax bracket

How much you could lose if Isa earnings were subject to income tax, broken down via interest rate and tax bracket

It is worth reiterating details of how Reeves may bring Isa interest into the Treasury’s taxable remit are not available.

GB News has applied latest income tax bands to these potential interest earnings.

Isas have revolutionised the savings market since they were introduced by Gordon Brown in 1999.

Latest figures show that 12.4 million adults were signed up for an Isa in 2022/23, a big increase on the 11.8 million the previous year.

A Treasury spokesman said: ‘We want to help people save for their future goals. We keep all aspects of savings policy under review.’