By Natalia Katona – May 14, 2026, 12:00 PM CDT

- Taiwan’s lost LNG supply from the Gulf turns a fuel disruption into a power-market risk, with more than 2 TWh of monthly gas-fired generation potentially exposed.

- Record US LNG deliveries are cushioning the immediate shock, but they replace stable baseload supply with costlier cargoes in an already tight Asian spot market.

- Coal can cover part of the gap and nuclear can help later, but Taiwan’s semiconductor-heavy economy is entering summer with a thinner energy buffer.

Taiwan’s LNG problem has turned from a diversification debate into an energy-security test. The island is 99% dependent on imported natural gas, and in 2025 roughly one-third of its 23.6 Mt of LNG imports came from the Gulf region – mostly from Qatar (almost 8 Mt) and another 200,000 t from the UAE. With Qatar’s gas production shut down and the Strait of Hormuz blocked, already loaded LNG tankers are trapped inside the Gulf. Taiwan received no LNG cargoes from Qatar or the UAE in April and May. For a country where gas-fired plants generate around half of all electricity, this is a direct hit to the fuel that was supposed to make Taiwan’s power system cleaner, flexible and secure.

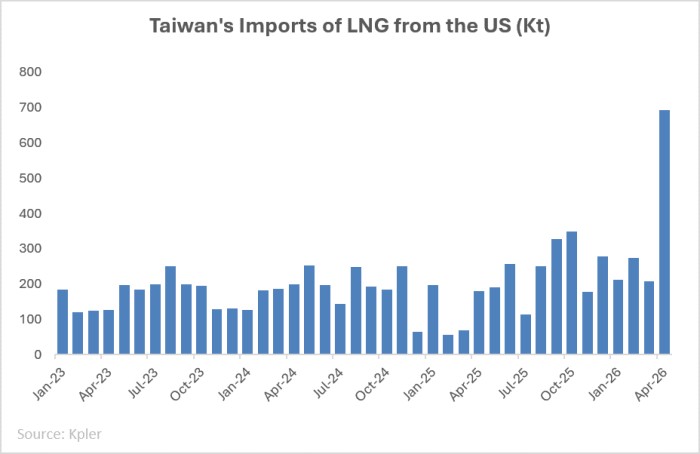

The shock has not yet shown up as an import collapse. Taiwan imported 1.9 Mt of LNG in April, broadly in line with a year earlier, though down from 2.03 Mt in March. That apparent stability in large originated from a record spike in US supply. American LNG deliveries rose from around 200,000 t in March to 700,000 t in April, the largest monthly volume of US LNG in Taiwan’s history. The US has become the emergency buffer, but emergency cargoes are not the same as a stable term supply. They are more expensive, more exposed to global bidding wars and less reliable than the cheaper Qatari volumes Taiwan had treated as part of its baseload procurement.

Australia is the other major pillar. Taiwan imported almost 8 Mt of Australian LNG in 2025, and this contract-secured imports level has been stable for the last three years. Yet it is not an unlimited backstop: Australia is also facing its own domestic gas-availability pressures and has introduced a rule requiring 20% of LNG export volumes to stay in the domestic market from 2027. Existing Taiwanese contracts signed before the December 22, 2025, cut-off are expected to be honoured (securing supplies to the island till September), but any near-term increase in Australian supply is realistically off the table.

CPC, Taiwan’s state-owned oil and gas company and its key LNG importer, is already trying to rebalance. Chairman Fang Jeng-zen said in early April that the company’s strategy was to reduce dependence on Middle Eastern LNG, with a new US contract bringing an additional 1.2 Mt annually. But that is a medium-term fix, not a quick replacement for lost Gulf cargoes. Russian LNG could be a practical answer, however Taiwan’s authorities see it differently. Taiwan bought four Yamal cargoes in 2025, totalling around 350,000 t, but has no plans to import Russian LNG now. Before the war in Ukraine, Taiwan had been a stable buyer of Russian LNG, taking around 1.8-2 Mt tonnes a year. That route is now politically constrained.

The power-market exposure is straightforward. Taiwan generated around 24.1 TWh of electricity per month in 2025, with gas-fired plants producing about 50% of it. Total LNG consumption was around 23.8 Mt, of which roughly 20 Mt went into power generation. That means about 85.5% of LNG use is tied directly to electricity production. If the lost Qatari and UAE cargoes are not replaced, and if no secure Gulf-origin LNG procurement is available from June, Taiwan could lose more than 2 TWh of gas-fired power generation per month – slightly less than 10% of monthly demand. That is large enough to force uncomfortable choices over who gets power first – especially in the face of a seasonal rise of electricity consumption from June till September.

Taiwan’s power-market structure gives the state control but not immunity. Government-owned Taipower controlled around 66% of power generation in 2025, while independent power producers generated the rest and sold electricity to Taipower. The system was built around a coal phase-down plan that, by 2025, should have left the mix at roughly 20% renewables, 30% coal and 50% gas, with no new coal-fired stations to be built. Coal was supposed to be displaced mainly by natural gas. Now the replacement fuel is the one in shortage.

That makes coal the obvious short-term fallback, like in many other countries in the Asia-Pacific region. Coal-fired generation now accounts for around 35% of Taiwan’s power output. Under the phase-down plan, four units at the Hsinda coal plant, with a combined capacity of around 2 GW, were moved into emergency back-up status between 2023 and 2025. They can now be used to offset part of the gas loss, with possible energy delivery assessed at around 1 TWh per month. That helps, but it covers only about half of the potential gas-fired generation gap.

Coal is also not an entirely problem-free option. Taiwan imported only 4.5 Mt of coal in April, the lowest in five years and down 5% year-on-year. More than half of Taiwan’s coal comes from Australia, including 2.4 Mt in April. FOB Newcastle prices have risen to $130/t, up 25% year-on-year. That is still far cheaper than LNG, but availability is tightening. Australia is producing around 38.5 Mt of coal a month and plans to ship around 37.5 Mt overseas, close to the limit of its capacity. China and Japan are also scrambling for alternatives to LNG, which means Taiwan is competing for the same coal cushion. It is expected to receive only slightly higher Australian volumes in May, according to Kpler, around 2.6 Mt. Taipower has been building coal inventories since January precisely in view of a potential LNG shortage, but inventories can buttress the system for only a brief period.

The bigger economic shift is Taiwan’s forced move deeper into spot LNG. Normally, around 70% of its LNG imports have been covered by term contracts, mainly from Qatar and Australia, while around 30% came from spot purchases. Losing oil-indexed Qatar volumes pushes Taiwan’s spot reliance to 60-65%. Landed Taiwan LNG prices, which used to hover around $10/MMBtu in February, are now around $17/MMBtu, with little prospect of quick relief. Taiwan can still buy cargoes, but it will do so in a market where every other Asian importer is also trying to insure itself against the same shortage.

Nuclear power should be the strategic fix to the island’s problems, but it cannot arrive in time. Taipower has submitted a plan to Taiwan’s Nuclear Safety Council to restart Kuosheng and Maanshan, two nuclear plants taken offline after their 40-year licences expired in 2023 and 2025, respectively. At full capacity, the four units could add around 30 TWh a year. That would be meaningful, but the full restart is unrealistic before 2028, leaving it irrelevant for the immediate summer squeeze.

So Taiwan is left with a fragile bridge: record US LNG, constrained Australian contracts, emergency coal-fired plants, and a nuclear option stuck in the future. Authorities say LNG imports have been secured on the spot market and through term Australian contracts until September. But media reports that official LNG reserves stood at only around 11 days of consumption in early May show how narrow the buffer is.

The danger extends beyond higher fuel prices, and not only for Taiwan itself. It revolves around power rationing in an economy built on semiconductor and photovoltaic manufacturing – two sectors of immense importance in a world that aspires to transition to cleaner energy options in the near future. If shortages hit in earnest, industry is likely to suffer first, as private consumers usually come as a priority for the authorities, causing a possible major semiconductor supply crisis globally. Taiwan’s energy transition has so far leaned on gas as a cleaner and more sustainable replacement for coal, but the Hormuz crisis is now exposing the risks in that bet.

By Natalia Katona for Oilprice.com

More Top Reads From Oilprice.com

- Two India-Bound LPG Tankers Clear Hormuz in Dark Mode

- India’s Wholesale Inflation Hits 3.5-Year High as Fuel Costs Surge 25%

- China Still Cautious on Fuel Shipments Despite Eased Export Rules

Download The Free Oilprice App Today

Natalia Katona

Natalia Katona is a freelance commodity analyst, based in the United Arab Emirates.